Strategy for UT Bot Alerts indicator Using the UT Bot alerts indicator by @QuantNomad, this strategy was designed for showing an example of how this indicator could be used, also, it has the goal to help some people from a group that use to use this indicator for their trading. Under any circumstance I recommend to use it without testing it before in real time.

Backtesting context: 2020-02-05 to 2023-02-25 of BTCUSD 4H by Tvc. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

UT Bot Alerts indicator by Quantnomad

One Ema of 200 periods for indicate the trend

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is higher than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as buy (open long position)

The other half will be closed when close price is lower than Atr and Ema from UT Bot cross under Atr. This will be showed as cl buy (close long position)

For shorts:

Close price is lower than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as sell (open short position)

The other half will be closed when close price is higher than Atr and Ema from UT Bot cross over Atr. This will be showed as cl sell (close short position)

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

---> Do not forget to deactivate Trades on chart option in style settings for a cleaner look of the chart <---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

---> The strategy can still be improved, you can change some parameters depending of the asset and timeframe like risk/reward for taking profits, for break even, also the main parameters of the UT Bot Alerts <----

Cerca negli script per "the strat"

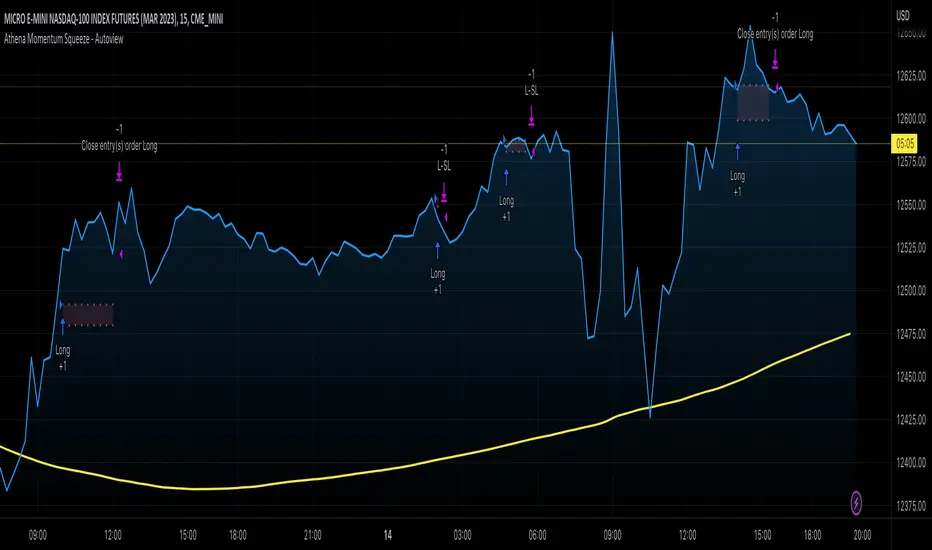

Athena Momentum Squeeze - Short, Lean, and Mean This is a very profitable strategy focusing on 15 minute intervals on the Micro Nasdaq Futures contracts. CME_MINI:MNQH2023

As this contract only keeps positions for on average about an hour risk is managed. At a profit factor of 3.382 with a max drawdown of $123 from January 1st to February 15. Looking back to Dec 2019 still maintains a profit factor of 1.3.

See backtesting: www.screencast.com

2019 backtesting: www.screencast.com

Based on the classic Lazy Bear Oscillator Squeeze with a number of modifications from ADX, MAs and adding fibonacci levels.

We like keeping strategies simple yet powerful, no completely where you can't understand your own trades.

Our team is always modifying and improving the strategy. Always open to collaborating on improving as there is no perfect strategy. www.screencast.com

Strategy Myth-Busting #11 - TrendMagic+SqzMom+CDV - [MYN]This is part of a new series we are calling "Strategy Myth-Busting" where we take open public manual trading strategies and automate them. The goal is to not only validate the authenticity of the claims but to provide an automated version for traders who wish to trade autonomously.

Our 11th one is an automated version of the "Magic Trading Strategy : Most Profitable Indicator : 1 Minute Scalping Strategy Crypto" strategy from "Fx MENTOR US" who doesn't make any official claims but given the indicators he was using, it looked like on the surface that this might actually work. The strategy author uses this on the 1 minute and 3 minute timeframes on mostly FOREX and Heiken Ashi candles but as the title of his strategy indicates is designed for Crypto. So who knows..

To backtest this accurately and get a better picture we resolved the Heiken Ashi bars to standard candlesticks . Even so, I was unable to sustain any consistency in my results on either the 1 or 3 min time frames and both FOREX and Crypto. 10000% Busted.

This strategy uses a combination of 3 open-source public indicators:

Trend Magic by KivancOzbilgic

Squeeze Momentum by LazyBear

Cumulative Delta Volume by LonesomeTheBlue

Trend Magic consists of two main indicators to validate momentum and volatility. It uses an ATR like a trailing Stop to determine the overarching momentum and CCI as a means to validate volatility. Together these are used as the primary indicator in this strategy. When the CCI is above 0 this is confirmation of a volatility event is occurring with affirmation based upon current momentum (ATR).

The CCI volatility indicator gets confirmation by the the Cumulative Delta Volume indicator which calculates the difference between buying and selling pressure. Volume Delta is calculated by taking the difference of the volume that traded at the offer price and the volume that traded at the bid price. The more volume that is traded at the bid price, the more likely there is momentum in the market.

And lastly the Squeeze Momentum indicator which uses a combination of Bollinger Bands, Keltner Channels and Momentum are used to again confirm momentum and volatility. During periods of low volatility, Bollinger bands narrow and trade inside Keltner channels. They can only contract so much before it can’t contain the energy it’s been building. When the Bollinger bands come back out, it explodes higher. When we see the histogram bar exploding into green above 0 that is a clear confirmation of increased momentum and volatile. The opposite (red) below 0 is true when there are low periods. This indicator is used as a means to really determine when there is premium selling plays going on leading to big directional movements again confirming the positive or negative momentum and volatility direction.

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

Trading Rules

1 - 3 min candles

FOREX or Crypto

Stop loss at swing high/low | 1.5 risk/ratio

Long Condition

Trend Magic line is Blue ( CCI is above 0) and above the current close on the bar

Squeeze Momentum's histogram bar is green/lime

Cumulative Delta Volume line is green

Short Condition

Trend Magic line is Red ( CCI is below 0) and below the current close on the bar

Squeeze Momentum's histogram bar is red/maroon

Cumulative Delta Volume line is peach

ATR PivotsThe "ATR Pivots" script is a technical analysis tool designed to help traders identify key levels of support and resistance on a chart. The indicator uses various metrics such as the Average True Range (ATR), Daily True Range ( DTR ), Daily True Range Percentage (DTR%), Average Daily Range (ADR), Previous Day High ( PDH ), and Previous Day Low ( PDL ) to provide a comprehensive picture of the volatility and movement of a security. The script also includes an EMA cloud and 200 EMA for trend identification and a 1-minute ATR scalping strategy for traders to make informed trading decisions.

ATR Detail:-

The ATR is a measure of the volatility of a security over a given period of time. It is calculated by taking the average of the true range (the difference between the high and low of a security) over a set number of periods. The user can input the number of periods (ATR length) to be used for the ATR calculation. The script also allows the user to choose whether to use the current close or not for the calculation. The script calculates various levels of support and resistance based on the relationship between the security's range ( high-low ) and the ATR. The levels are calculated by multiplying the ATR by different Fibonacci ratios (0.236, 0.382, 0.5, 0.618, 0.786, 1.000) and then adding or subtracting the result from the previous close. The script plots these levels on the chart, with the -100 level being the most significant level. The user also has an option to choose whether to plot all Fibonacci levels or not.

DTR and DTR% Detail:-

The Daily True Range Percentage (DTR%) is a metric that measures the daily volatility of a security as a percentage of its previous close. It is calculated by dividing the Daily True Range ( DTR ) by the previous close. DTR is the range between the current period's high and low and gives a measure of the volatility of the security on a daily basis. DTR% can be used as an indicator of the percentage of movement of the security on a daily basis. In this script, DTR% is used in combination with other metrics such as the Average True Range (ATR) and Fibonacci ratios to calculate key levels of support and resistance for the security. The idea behind using DTR% is that it can help traders to better understand the daily volatility of the security and make more informed trading decisions.

For example, if a security has a DTR% of 2%, it suggests that the security has a relatively low level of volatility and is less likely to experience significant price movements on a daily basis. On the other hand, if a security has a DTR% of 10%, it suggests that the security has a relatively high level of volatility and is more likely to experience significant price movements on a daily basis.

ADR:-

The script then calculates the ADR (Average Daily Range) which is the average of the daily range of the security, using the formula (Period High - Period Low) / ATR Length. This gives a measure of the average volatility of the security on a daily basis, which can be useful for determining potential levels of support and resistance .

PDH /PDL:-

The script also calculates PDH (Previous Day High) and PDL (Previous Day Low) which are the High and low of the previous day of the security. This gives a measure of the previous day's volatility and movement, which can be useful for determining potential levels of support and resistance .

EMA Cloud and 200 EMA Detail:-

The EMA cloud is a technical analysis tool that helps traders identify the trend of the market by comparing two different exponential moving averages (EMAs) of different lengths. The cloud is created by plotting the fast EMA and the slow EMA on the chart and filling the space between them. The user can input the length of the fast and slow EMA , and the script will calculate and plot these EMAs on the chart. The space between the two EMAs is then filled with a color that represents the trend, with green indicating a bullish trend and red indicating a bearish trend . Additionally, the script also plots a 200 EMA , which is a commonly used long-term trend indicator. When the fast EMA is above the slow EMA and the 200 EMA , it is considered a bullish signal, indicating an uptrend. When the fast EMA is below the slow EMA and the 200 EMA , it is considered a bearish signal, indicating a downtrend. The EMA cloud and 200 EMA can be used together to help traders identify the overall trend of the market and make more informed trading decisions.

1 Minute ATR Scalping Strategy:-

The script also includes a 1-minute ATR scalping strategy that can be used by traders looking for quick profits in the market. The strategy involves using the ATR levels calculated by the script as well as the EMA cloud and 200 EMA to identify potential buy and sell opportunities. For example, if the 1-minute ATR is above 11 in NIFTY and the EMA cloud is bullish , the strategy suggests buying the security. Similarly, if the 1-minute ATR is above 30 in BANKNIFTY and the EMA cloud is bullish , the strategy suggests buying the security.

Inside Candle:-

The Inside Candle is a price action pattern that occurs when the current candle's high and low are entirely within the range of the previous candle's high and low. This pattern indicates indecision or consolidation in the market and can be a potential sign of a trend reversal. When used in the 15-minute chart, traders can look for Inside Candle patterns that occur at key levels of support or resistance. If the Inside Candle pattern occurs at a key level and the price subsequently breaks out of the range of the Inside Candle, it can be a signal to enter a trade in the direction of the breakout. Traders can also use the Inside Candle pattern to trade in a tight range, or to reduce their exposure to a current trend.

Risk Management:-

As with any trading strategy, it is important to practice proper risk management when using the ATR Pivots script and the 1-minute ATR scalping strategy. This may include setting stop-loss orders, using appropriate position sizing, and diversifying your portfolio. It is also important to note that past performance is not indicative of future results and that the script and strategy provided are for educational purposes only.

In conclusion, the "ATR Pivots" script is a powerful tool that can help traders identify key levels of support and resistance , as well as trend direction. The additional metrics such as DTR , DTR%, ADR, PDH , and PDL provide a more comprehensive picture of the volatility and movement of the security, making it easier for traders to make better trading decisions. The inclusion of the EMA cloud and 200 EMA for trend identification, and the 1-minute ATR scalping strategy for quick profits can further enhance a trader's decision-making process. However, it is important to practice proper risk management and understand that past performance is not indicative of future results.

Special thanks to satymahajan for the idea of clubbing Average True Range with Fibonacci levels.

Simple SuperTrend Strategy for BTCUSD 4HHello guys!, If you are a swing trader and you are looking for a simple trend strategy, you should check this one. Based in the supertrend indicator, this strategy will help you to catch big movements in BTCUSD 4H and avoid losses as much as possible in consolidated situations of the market

This strategy was designed for BTCUSD in 4H timeframe

Backtesting context: 2020-01-02 to 2023-01-05 (The strategy has also worked in previous years)

Trade conditions:

Rules are actually simple, the most important thing is the risk and position management of this strategy

For long:

Once Supertrend changes from a downtrend to a uptrend, you enter into a long position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Now, just will be there two situations:

Once Supertrend changes from a uptrend to a downtrend, you close the other half of the initial long position.

If price goes againts the position, the position will be closed due to breakeven.

For short:

Once Supertrend changes from a uptrend to a downtrend, you enter into a short position. The stop loss will be defined by the atr stop loss

The first profit will be of 0.75 risk/reward ratio where half position will be closed. When this happens, you move the stop loss to break even.

Like in the long position, just will be there two situations:

Once Supertrend changes from a downtrend to a uptrend, you close the other half of the initial short position.

If price goes againts the position, the position will be closed due to breakeven.

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, supertrend or positions.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

Signals meanings:

L for long position. CL for close long position.

S for short position. CS for close short position.

Tp for take profit (it also appears when the position is closed due to stop loss, this due to the script uses two kind of positions)

Exit due to break even or due to stop loss

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

The amount of trades closed in the backtest are not exactly the real ones. If you want to know the real ones, go to settings and change % of trade for first take profit to 100 for getting the real ones. In the backtest, the real amount of opened trades was of 194.

Indicators used:

Supertrend

Atr stop loss by garethyeo

This is the fist strategy that I publish in tradingview, I will be glad with you for any suggestion, support or advice for future scripts. Do not doubt in make any question you have and if you liked this content, leave a boost. I plan to bring more strategies and useful content for you!

Big Poppa Code Strat & Momentum Strategy IndicatorThis indicator is a combination of a few things in order to work with a unique trading style gleaned from Callme100k, jrgreatness, TrustMyLevels , FaithInTheStrat, Rob Smith and Saty Mahajan.

This Indicator is created to help you day trade using, ATR Fibonacci Levels, Price Action and Momentum.

It displays Fibonacci Levels Based on ATR to indicate when a security is 0.236, 0.382 +- the Days Open, +- the Days Open, 0.618 +- the Days Open and 1.0 +- Days Open.

To understand this script you need to understand

Average True Range (ATR)

1 Bar Inside Bar

2 Bar Outside Bar (Break either the top or bottom)

3 Bar Engulfing Bar

Strat Setups - 212, 322, 312

Fibonacci - 0.236, 0.382, 0.618, 1.0

Moving Averages

A Trend is considered bullish when (green)

Current Price is greater than the Fast EMA Value (8)

Fast EMA is greater than PIVOT EMA Value (21)

Pivot EMA is greater than SLOW EMA Value (34)

OR Hull is trending up and the Price is above the Volume Weighted Moving Average and price is above VWAP

A trend is considered Bearish when (red)

Current Price is less than the Fast EMA Value (8)

Fast EMA is less than PIVOT EMA Value (21)

Pivot EMA is less than SLOW EMA Value (34)

OR Hull is trending down and the Price is below the Volume Weighted Moving Average and price is below VWAP

If these conditions are not met then the Momentum is in Conflict (orange)

The Momentum band will match the color of the current trend

The table that is present can be turned off at any time lets you see

1) If Moving Averages are showing bullish, bearish or in conflict

2) If There us Time Frame Continuity, (if 5 min up, are all the other timeframes up also)

3) How much of the ATR have we moved on the day

4) Are we in Call or Put range for the day based on ATR Fib Levels

The Ideal situation for entering a call

1) Momentum is Green

2) FTFC on Green

3) A Strat Actionable Signal is present

4) You are in the call range, 0.236 - 0.618 ATR + the Price

5) The ATR still has room, I.e only 50% of the ATR has been run already

Ideal situation from entering a put

1) Momentum is red

2) FTFC on Red

3) A Strat Actionable Signal is present

4) You are in the put range, 0.236 - 0.618 ATR - the Price

5) The ATR still has room, I.e only 50% of the ATR has been run already

Exit the trade for these reasons you entered (for profit or loss)

1) ATR has no more room

2) FTFC is now in conflict

3) Momentum has shifted

Take Profit when

1) You reach a new ATR Level 0.618, 1.0 , -0.618, -1, etc

Passive Stop Loss

1) Open Price if you are aggressive

2) Next ATR Level Down or Up

Feel free to take profit and leave runners

This script does not give signals, you should do your own research, I am not a financial advisors, I am simply applying principles of seasoned veterans to code. You make all decisions about how you buy, sell and trade. The creator of this script makes no promises and takes no responsibility for your personal trading.

To research the methods described above look up

Rob Smith : The Strat

Saty Mahajan : ATR Levels

Fibonacci

Using the HULL Moving Average

Exponential Moving Averages

VWAP

VWMA

RSI Divergence Strategywhat is "RSI Divergence Strategy"?

it is a RSI strategy based this indicator:

what it does?

it gives buy or sell signals according to RSI Divergences. it also has different variables such as "take profit", "stop loss" and trailing stop loss.

how it does it?

it uses the "RSI Divergence" indicator to give signal. For detailed information on how it works, you can visit the link above. The quantity of the inputs is proportional to the rsi values. Long trades are directly traded with "RSI" value, while short poses are traded with "100-RSI" value.

How to use it?

The default settings are for scalp strategy but can be used for any type of trading strategy. you can develop different strategies by changing the sections. It is quite simple to use.

RSI length is length of RSİ

source is source of RSİ

RSİ Divergence lenght is length of line on the RSI

The "take profit", "stop" and "trailing stop" parts used in the "buy" group only affect buys. The "sell" group is similarly independent of the variables in the "buy" group.

The "zoom" section is used to enlarge or reduce the indicator. it only changes the appearance, it does not affect the results of the strategy.

Fibonacci Zones EMA Zones StrategyThis idea is only for fun and learning purposes only.

The strategy represents 2 simple math formulas that are very simple. the "Fibo Formula" and the "EMA Formula" Please see source code for reference

I Feel like coders can learn a lot about developing strategies using this source code

This is to show that there is unlimited amount of variables and factors to a strategy and its all about working with probability.

Also to show that unlimited amount of conditions could be added to a strategy.

And unlimited amount of variables/factors with the settings that could change the results.

Rules are simple

Entry on close, Close/Entry must be in the blue Fibo Zone

Blue Fibonacci zone fully customizable

Other Conditions could be added involving EMA zones, Over Ema1, Under Ema1 etc..

TP/SL and Dates Fully Customizable

This script is just an idea fully for learning purposes.

EMA RSI Strategy

Simple strategy

=============

If the last two closes are in ascending order, the rsi is below 50 and ascending, and the current candle is above 200 ema, then LONG. If the last two closes are in descending order, the rsi is above 50 and descending, and the current candle is below 200 ema, then SHORT.

LONG Exit strategy:

ATR: Last 14 day

Lowest: The lowest value of the last 14 candles

Limit points = (Trade Price - Lowest + ATR) * 100000

trail_points : Limit/2

trail_offset = Limit/2

SHORT Exit strategy:

ATR: Last 14 day

Highest: The higher value of the last 14 candles

Limit points = (Trade Price - Highest + ATR) * 100000

trail_points : Limit/2

trail_offset = Limit/2

Backtest results for the AUDUSD pair gave positive results over the last three months.

I am testing this strategy using a python bot in a real environment this week and will update the results at the end of the week.

Disclaimer

This is not financial advice. You should seek independent advice to check how the strategy information relates to your unique circumstances.

We are not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly by this strategy.

Heikin Ashi SupertrendAbout this Strategy

This supertrend strategy uses the Heikin Ashi candles to generate the supertrend but enters and exits trades using normal candle close prices. If you use the standard built in Supertrend indicator on Heikin Ashi candles, it will produce very unrealistic backtesting results because it uses the Heikin Ashi prices instead of the real prices. However, by signaling the supertrend reversals using Heikin Ashi while using standard candle close prices for the entries and exits, it corrects the backtesting errors and gives you a more realistic equity curve. You should set the chart to use standard candles and then hide them (the strategy creates the candles).

This strategy includes:

Plotting of Heikin Ashi candles

Heikin Ashi Supertrend

Long and Short Entry Signals

Move stop loss after trade is X% in profit

Profit Target

Stop Loss

Built in Alertatron automation

Alertatron Trade Automation Integration

For Alertatron integration, be sure to configure the strategy settings and "Enable Webhook Messages" before creating an alert with {{strategy.order.alert_message}} in the body of your alert message. Be sure to enable webhooks and point it to your Incoming Alertatron webhook URL.

Notes

While this strategy does pretty well during trending markets, It's worth noting that the Buy and Hold ROI is much better during peak times of the bull market

Not financial advice. Do not risk more than you can afford to lose.

Multi Trend Cross Strategy TemplateToday I am sharing with the community trend cross strategy template that incorporates any combination of over 20 built in indicators. Some of these indicators are in the Pine library, and some have been custom coded and contributed over time by the beloved Pine Coder community. Identifying a trend cross is a common trend following strategy and a common custom-code request from the community. Using this template, users can now select from over 400 different potential trend combinations and setup alerts without any custom coding required. This Multi-Trend cross template has a very inclusive library of trend calculations/indicators built-in, and will plot any of the 20+ indicators/trends that you can select in the settings.

How it works : Simple trend cross strategies go long when the fast trend crosses over the slow trend, and/or go short when the fast trend crosses under the slow trend. Options for either trend direction are built-in to this strategy template. The script is also coded in a way that allows you to enable/modify pyramid settings and scale into a position over time after a trend has crossed.

Use cases : These types of strategies can reduce the volatility of returns and can help avoid large market downswings. For instance, those running a longer term trend-cross strategy may have not realized half the down swing of the bear markets or crashes in 02', 08', 20', etc. However, in other years, they may have exited the market from time to time at unfavorable points that didn't end up being a down turn, or at times the market was ranging sideways. Some also use them to reduce volatility and then add leverage to attempt to beat buy/hold of the underlying asset within an acceptable drawdown threshold.

Special thanks to @Duyck, @everget, @KivancOzbilgic and @LazyBear for coding and contributing earlier versions of some of these custom indicators in Pine.

This script incorporates all of the following indicators. Each of them can be selected and modified from within the indicator settings:

ALMA - Arnaud Legoux Moving Average

DEMA - Double Exponential Moving Average

DSMA - Deviation Scaled Moving Average - Contributed by Everget

EMA - Exponential Moving Average

HMA - Hull Moving Average

JMA - Jurik Moving Average - Contributed by Everget

KAMA - Kaufman's Adaptive Moving Average - Contributed by Everget

LSMA - Linear Regression , Least Squares Moving Average

RMA - Relative Moving Average

SMA - Simple Moving Average

SMMA - Smoothed Moving Average

Price Source - Plotted based on source selection

TEMA - Triple Exponential Moving Average

TMA - Triangular Moving Average

VAMA - Volume Adjusted Moving Average - Contributed by Duyck

VIDYA - Variable Index Dynamic Average - Contributed by KivancOzbilgic

VMA - Variable Moving Average - Contributed by LazyBear

VWMA - Volume Weighted Moving Average

WMA - Weighted Moving Average

WWMA - Welles Wilder's Moving Average

ZLEMA - Zero Lag Exponential Moving Average - Contributed by KivancOzbilgic

Disclaimer : This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Channels Strategy [JoseMetal]============

ENGLISH

============

- Description:

This strategy is based on Bollinger Bands / Keltner Channel price "rebounds" (the idea of price bouncing from one band to another).

The strategy has several customizable options, which allows you to refine the strategy for your asset and timeframe.

You can customize settings for ALL indicators, Bollinger Bands (period and standard deviation), Keltner Channel (period and ATR multiplier) and ATR (period).

- AVAILABLE INDICATORS:

You can pick Bollinger Bands or Keltner Channels for the strategy, the chosen indicator will be plotted as well.

- CUSTOM CONDITIONS TO ENTER A POSITION:

1. Price breaks the band (low below lower band for LONG or high above higher band for SHORT).

2. Same as 1 but THEN (next candle) price closes INSIDE the bands.

3. Price breaks the band AND CLOSES OUT of the band (lower band for LONG and higher band for SHORT).

4. Same as 3 but THEN (next candle) price closes INSIDE the bands.

- STOP LOSS OPTIONS:

1. Previous wick (low of previous candle if LONG and high or previous candle if SHORT).

2. Extended band, you can customize settings for a second indicator with larger values to use it as STOP LOSS, for example, Bollinger Bands with 2 standard deviations to open positions and 3 for STOP LOSS.

3. ATR: you can pick average true ratio from a source (like closing price) with a multiplier to calculate STOP LOSS.

- TAKE PROFIT OPTIONS:

1. Opposite band (top band for LONGs, bottom band for SHORTs).

2. Moving average: Bollinger Bands simple moving average or Keltner Channel exponential moving average .

3. ATR: you can pick average true ratio from a source (like closing price) with a multiplier to calculate TAKE PROFIT.

- OTHER OPTIONS:

You can pick to trade only LONGs, only SHORTs, both or none (just indicator).

You can enable DYNAMIC TAKE PROFIT, which updates TAKE PROFIT on each candle, for example, if you pick "opposite band" as TAKE PROFIT, it'll update the TAKE PROFIT based on that, on every single new candle.

- Visual:

Bands shown will depend on the chosen indicator and it's settings.

ATR is only printed if used as STOP LOSS and/or TAKE PROFIT.

- Recommendations:

Recommended on DAILY timeframe , it works better with Keltner Channels rather than Bollinger Bands .

- Customization:

As you can see, almost everything is customizable, for colors and plotting styles check the "Style" tab.

Enjoy!

============

ESPAÑOL

============

- Descripción:

Esta estrategia se basa en los "rebotes" de precios en las Bandas de Bollinger / Canal de Keltner (la idea de que el precio rebote de una banda a otra).

La estrategia tiene varias opciones personalizables, lo que le permite refinar la estrategia para su activo y temporalidad favoritas.

Puedes personalizar la configuración de TODOS los indicadores, Bandas de Bollinger (periodo y desviación estándar), Canal de Keltner (periodo y multiplicador ATR) y ATR (periodo).

- INDICADORES DISPONIBLES:

Puedes elegir las Bandas de Bollinger o los Canales de Keltner para la estrategia, el indicador elegido será mostrado en pantalla.

- CONDICIONES PERSONALIZADAS PARA ENTRAR EN UNA POSICIÓN:

1. El precio rompe la banda (mínimo por debajo de la banda inferior para LONG o máximo por encima de la banda superior para SHORT).

2. Lo mismo que en el punto 1 pero ADEMÁS (en la siguiente vela) el precio cierra DENTRO de las bandas.

3. El precio rompe la banda Y CIERRA FUERA de la banda (banda inferior para LONG y banda superior para SHORT).

4. Igual que el 3 pero ADEMÁS (siguiente vela) el precio cierra DENTRO de las bandas.

- OPCIONES DE STOP LOSS:

1. Mecha anterior (mínimo de la vela anterior si es LONGy máximo de la vela anterior si es SHORT).

2. Banda extendida, puedes personalizar la configuración de un segundo indicador con valores más extensos para utilizarlo como STOP LOSS, por ejemplo, Bandas de Bollinger con 2 desviaciones estándar para abrir posiciones y 3 para STOP LOSS.

3. ATR: puedes elegir el average true ratio de una fuente (como el precio de cierre) con un multiplicador para calcular el STOP LOSS.

- OPCIONES DE TAKE PROFIT:

1. Banda opuesta (banda superior para LONGs, banda inferior para SHORTs).

2. Media móvil: media móvil simple de las Bandas de Bollinger o media móvil exponencial del Canal de Keltner .

3. ATR: se puede escoger el average true ratio de una fuente (como el precio de cierre) con un multiplicador para calcular el TAKE PROFIT.

- OTRAS OPCIONES:

Puedes elegir operar sólo con LONGs, sólo con SHORTs, ambos o ninguno (sólo el indicador).

Puedes activar el TAKE PROFIT DINÁMICO, que actualiza el TAKE PROFIT en cada vela, por ejemplo, si eliges "banda opuesta" como TAKE PROFIT, actualizará el TAKE PROFIT basado en eso, en cada nueva vela.

- Visual:

Las bandas mostradas dependerán del indicador elegido y de su configuración.

El ATR sólo se muestra si se utiliza como STOP LOSS y/o TAKE PROFIT.

- Recomendaciones:

Recomendada para temporalidad de DIARIO, funciona mejor con los Canales de Keltner que con las Bandas de Bollinger .

- Personalización:

Como puedes ver, casi todo es personalizable, para los colores y estilos de dibujo comprueba la pestaña "Estilo".

¡Que lo disfrutes!

[Sniper] SuperTrend + SSL Hybrid + QQE MODHi. I’m DuDu95.

**********************************************************************************

This is the script for the series called "Sniper".

*** What is "Sniper" Series? ***

"Sniper" series is the project that I’m going to start.

In "Sniper" Series, I’m going to "snipe and shoot" the youtuber’s strategy: to find out whether the youtuber’s video about strategy is "true or false".

Specifically, I’m going to do the things below.

1. Implement "Youtuber’s strategy" into pinescript code.

2. Then I will "backtest" and prove whether "the strategy really works" in the specific ticker (e.g. BTCUSDT) for the specific timeframe (e.g. 5m).

3. Based on the backtest result, I will rate and judge whether the youtube video is "true" or "false", and then rate the validity, reliability, robustness, of the strategy. (like a lie detector)

*** What is the purpose of this series? ***

1. To notify whether the strategy really works for the people who watched the youtube video.

2. To find and build my own scalping / day trading strategy that really works.

**********************************************************************************

*** Strategy Description ***

This strategy is from " QQE MOD + supertrend + ssl hybrid" by korean youtuber "코인투데이".

"코인투데이" claimed that this strategy will make you a lot of money in any crypto ticker in 15 minute timeframe.

### Entry Logic

1. Long Entry Logic

- Super Trend Short -> Long

- close > SSL Hybrid baseline upper k

- QQE MOD should be blue

2. Short Entry Logic

- Super Trend Long -> Short

- close < SSL Hybrid baseline lower k

- QQE MOD should be red

### Exit Logic

1. Long Exit Logic

- Super Trend Long -> Short

2. Short Entry Logic

- Super Trend Short -> Long

### StopLoss

1. Can Choose Stop Loss Type: Percent, ATR, Previous Low / High.

2. Can Chosse inputs of each Stop Loss Type.

### Take Profit

1. Can set Risk Reward Ratio for Take Profit.

- To simplify backtest, I erased all other options except RR Ratio.

- You can add Take Profit Logic by adding options in the code.

2. Can set Take Profit Quantity.

### Risk Manangement

1. Can choose whether to use Risk Manangement Logic.

- This controls the Quantity of the Entry.

- e.g. If you want to take 3% risk per trade and stop loss price is 6% below the long entry price,

then 50% of your equity will be used for trade.

2. Can choose How much risk you would take per trade.

### Plot

1. Added Labels to check the data of entry / exit positions.

2. Changed and Added color different from the original one. (green: #02732A, red: #D92332, yellow: #F2E313)

3. SuperTrend and SSL Hybrid Baseline is by default drawn on the chart.

4. If you check EMA filter, EMA would be drawn on the chart.

5. Should add QQE MOD indicator manually if you want to see QQE MOD.

**********************************************************************************

*** Rating: True or False?

### Rating:

→ 3.5 / 5 (0 = Trash, 1 = Bad, 2 = Not Good, 3 = Good, 4 = Great, 5 = Excellent)

### True or False?

→ True but not a 'perfect true'.

→ It did made a small profit on 15 minute timeframe. But it made a profit so it's true.

→ It worked well in longer timeframe. I think super trend works well so I will work on this further.

### Better Option?

→ Use this for Day trading or Swing Trading, not for Scalping. (Bigger Timeframe)

→ Although the result was not good at 15 minute timeframe, it was quite profitable in 1h, 2h, 4h, 8h, 1d timeframe.

→ Crypto like BTC, ETH was ok.

→ The result was better when I use EMA filter.

### Robust?

→ Yes. Although result was super bad in 5m timeframe, backtest result was "consistently" profitable on longer timeframe (when timeframe was bigger than 15m, it was profitable).

→ Also, MDD was good under risk management option on.

**********************************************************************************

*** Conclusion?

→ I recommend you not to use this on short timeframe as the youtuber first mentioned.

→ In my opinion, I can use on longer timeframe like 2h or bigger with EMA filter, stoploss and risk management.

[Sniper] SSL Hybrid + QQE MOD + Waddah Attar StrategyHi. I’m DuDu95.

**********************************************************************************

This is the script for the series called "Sniper".

*** What is "Sniper" Series? ***

"Sniper" series is the project that I’m going to start.

In "Sniper" Series, I’m going to "snipe and shoot" the youtuber’s strategy: to find out whether the youtuber’s video about strategy is "true or false".

Specifically, I’m going to do the things below.

1. Implement "Youtuber’s strategy" into pinescript code.

2. Then I will "backtest" and prove whether "the strategy really works" in the specific ticker (e.g. BTCUSDT) for the specific timeframe (e.g. 5m).

3. Based on the backtest result, I will rate and judge whether the youtube video is "true" or "false", and then rate the validity, reliability, robustness, of the strategy. (like a lie detector)

*** What is the purpose of this series? ***

1. To notify whether the strategy really works for the people who watched the youtube video.

2. To find and build my own scalping / day trading strategy that really works.

**********************************************************************************

*** Strategy Description ***

This strategy is from "SSL QQE MOD 5MIN SCALPING STRATEGY" by youtuber "Daily Investments".

"Daily Investments" claimed that this strategy will make you some money from 100 trades in any ticker in 5 minute timeframe.

### Entry Logic

1. Long Entry Logic

- close > SSL Hybrid Baseline.

- QQE MOD should turn into blue color.

- Waddah Attar Explosion indicator must be green.

2. Short Entry Logic

- close < SSL Hybrid Baseline

- QQE MOD should turn into red color.

- Waddah Attar Explosion indicator must be red.

### Exit Logic

1. Long Exit Logic

- When QQE MOD turn into red color.

2. Short Entry Logic

- When QQE MOD turn into blue color.

### StopLoss

1. Can Choose Stop Loss Type: Percent, ATR, Previous Low / High.

2. Can Chosse inputs of each Stop Loss Type.

### Take Profit

1. Can set Risk Reward Ratio for Take Profit.

- To simplify backtest, I erased all other options except RR Ratio.

- You can add Take Profit Logic by adding options in the code.

2. Can set Take Profit Quantity.

### Risk Manangement

1. Can choose whether to use Risk Manangement Logic.

- This controls the Quantity of the Entry.

- e.g. If you want to take 3% risk per trade and stop loss price is 6% below the long entry price,

then 50% of your equity will be used for trade.

2. Can choose How much risk you would take per trade.

### Plot

1. Added Labels to check the data of entry / exit positions.

2. Changed and Added color different from the original one. (green: #02732A, red: #D92332, yellow: #F2E313)

3. SSL Hybrid Baseline is by default drawn on the chart.

4. If you check EMA filter, EMA would be drawn on the chart.

5. Should add QQE MOD and Waddah Attar Explosion indicator manually if you want to see QQE MOD.

**********************************************************************************

*** Rating: True or False?

### Rating:

→ 1.5 / 5 (0 = Trash, 1 = Bad, 2 = Not Good, 3 = Good, 4 = Great, 5 = Excellent)

### True or False?

→ False

→ Doesn't Work on 5 minute timeframe. Also, it doesn't work on crypto.

### Better Option?

→ Use this for Day trading or Swing Trading, not for Scalping. (Bigger Timeframe)

→ Although the result was bad at 5 minute timeframe, it was profitable in 1h, 2h, 4h, 8h, 1d timeframe.

→ BTC, ETH was ok.

→ The result was better when I use EMA filter (only on longer timeframe).

### Robust?

→ So So. Although result was bad in short timeframe (e.g. 30m 15m 5m), backtest result was "consistently" profitable on longer timeframe.

→ Also, MDD was not that bad under risk management option on.

**********************************************************************************

*** Conclusion?

→ Don't use this on short timeframe.

→ Better use on longer timeframe with filter, stoploss and risk management.

Strategy PnL LibraryLibrary "Strategy_PnL_Library"

TODO: This is a library that helps you learn current pnl of open position and use it to create your own dynamic take profit or stop loss rules based on current level of your profit. It should only be used with strategies.

inTrade()

inTrade: Checks if a position is currently open.

Returns: bool: true for yes, false for no.

notInTrade()

inTrade: Checks if a position is currently open. Interchangeable with inTrade but just here for simple semantics.

Returns: bool: true for yes, false for no.

pnl()

pnl: Calculates current profit or loss of position after the commission. If the strategy is not in trade it will always return na.

Returns: float: Current Profit or Loss of position, positive values for profit, negative values for loss.

entryBars()

entryBars: Checks how many bars it's been since the entry of the position.

Returns: int: Returns a int of strategy entry bars back. Minimum value is always corrected to 1 to avoid lookback errors.

pnlvelocity()

pnlvelocity: Calculates the velocity of pnl by following the change in open profit compared to previous bar. If the strategy is not in trade it will always return na.

Returns: float: Returns a float value of pnl velocity.

pnlacc()

pnlacc: Calculates the acceleration of pnl by following the change in profit velocity compared to previous bar. If the strategy is not in trade it will always return na.

Returns: float: Returns a float value of pnl acceleration.

pnljerk()

pnljerk: Calculates the jerk of pnl by following the change in profit acceleration compared to previous bar. If the strategy is not in trade it will always return na.

Returns: float: Returns a float value of pnl jerk.

pnlhigh()

pnlhigh: Calculates the highest value the pnl has reached since the start of the current position. If the strategy is not in trade it will always return na.

Returns: float: Returns a float highest value the pnl has reached.

pnllow()

pnllow: Calculates the lowest value the pnl has reached since the start of the current position. If the strategy is not in trade it will always return na.

Returns: float: Returns a float lowest value the pnl has reached.

pnldev()

pnldev: Calculates the deviance of the pnl since the start of the current position. If the strategy is not in trade it will always return na.

Returns: float: Returns a float deviance value of the pnl.

pnlvar()

pnlvar: Calculates the variance value of the pnl since the start of the current position. If the strategy is not in trade it will always return na.

Returns: float: Returns a float variance value of the pnl.

pnlstdev()

pnlstdev: Calculates the stdev value of the pnl since the start of the current position. If the strategy is not in trade it will always return na.

Returns: float: Returns a float stdev value of the pnl.

pnlmedian()

pnlmedian: Calculates the median value of the pnl since the start of the current position. If the strategy is not in trade it will always return na.

Returns: float: Returns a float median value of the pnl.

Monthly Returns of a Strategy in a ChartIt's a simple example of how you can present your strategy's monthly performance in a chart.

You maybe know that there is no support of these kind of charts in TradingView so this chart is actually a table object under the hood.

Table visual appearance is customizable, you can change:

Location

Bar Width / High

Colors

Thanks to @MUQWISHI for hard work, for helping me coding it.

It's not about the strategy itself but the way you display returns on your chart. So pls don't critique my choice of the strategy and its performance 🙂

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

ALMA/EMA/SRSI Strategy + IndicatorBack with another great high hit rate strategy!!

Disclaimer* This strategy was sampled using source code written by @ClassicScott , as referred to in the script, there is a clear line where the source code was scripted by myself.

This Strategy consists of three key factors, the ALMA, EMA crossover, and a Stochastic Rsi

ALMA: The Alma is the step line shown, turning green and red at select times. This average value gives general oversight of the macro movement of price action. and this particular one was coded by Mr.ClassicScott.

EMA crossover: At the input screen you are given an option of the fast and slow ema's. The default is solely for the hit rate and correlation to the Alma of this strategy. The arrows you see depicted on the chart are the crossover events happening.

Stochastic Rsi: The Stochastic Rsi is a stochastic value, using data sampled from the rsi. The use of this indicator in my strategy is to prevent entries when too overbought and oversold, as well as closures and vice versa, to prevent holding bags either way.

Fixed % TP: In the input screen you are given a take profit and stop loss percentage, for good R/R the hit rate will take a notch down, but with no R/R it will be near perfect.

How to use this:

Add it to your chart to get the strategy inputs. (The strategy is really only useful on a 15min TF. However the indicator within it can be used on anything at anytime!)

Watch the yellow and aqua moving averages, these are your ema's and crossover's will trigger signals based on your integer inputs.

Find Correlation between other leading indicators, as well as crossover's down/up and a red/green alma.

DO NOT use the arrows as buy/sell signals. These are simply to show ema's are crossing under or over. Momentum indicator's paired with this can be useful to determine if it could be a buy signal or sell signal.

Cheat Code's Notes:

Almost at 1000 boosts!!! I appreciate the support from everyone and I will keep trying my best to deliver quality strategies for the people.

-Cheat Code

BYBIT:BTCUSDT

Smoothed Heikin Ashi Trend on Chart - TraderHalai BACKTESTSmoothed Heikin Ashi Trend on chart - Backtest

This is a backtest of the Smoothed Heikin Ashi Trend indicator, which computes the reverse candle close price required to flip a Heikin Ashi trend from red to green and vice versa. The original indicator can be found in the scripts section of my profile.

This particular back test uses this indicator with a Trend following paradigm with a percentage-based stop loss.

Note, that backtesting performance is not always indicative of future performance, but it does provide some basis for further development and walk-forward / live testing.

Testing was performed on Bitcoin , as this is a primary target market for me to use this kind of strategy.

Sample Backtesting results as of 10th June 2022:

Backtesting parameters:

Position size: 10% of equity

Long stop: 1% below entry

Short stop: 1% above entry

Repainting: Off

Smoothing: SMA

Period: 10

8 Hour:

Number of Trades: 1046

Gross Return: 249.27 %

CAGR Return: 14.04 %

Max Drawdown: 7.9 %

Win percentage: 28.01 %

Profit Factor (Expectancy): 2.019

Average Loss: 0.33 %

Average Win: 1.69 %

Average Time for Loss: 1 day

Average Time for Win: 5.33 days

1 Day:

Number of Trades: 429

Gross Return: 458.4 %

CAGR Return: 15.76 %

Max Drawdown: 6.37 %

Profit Factor (Expectancy): 2.804

Average Loss: 0.8 %

Average Win: 7.2 %

Average Time for Loss: 3 days

Average Time for Win: 16 days

5 Day:

Number of Trades: 69

Gross Return: 1614.9 %

CAGR Return: 26.7 %

Max Drawdown: 5.7 %

Profit Factor (Expectancy): 10.451

Average Loss: 3.64 %

Average Win: 81.17 %

Average Time for Loss: 15 days

Average Time for Win: 85 days

Analysis:

The strategy is typical amongst trend following strategies with a less regular win rate, but where profits are more significant than losses. Most of the losses are in sideways, low volatility markets. This strategy performs better on higher timeframes, where it shows a positive expectancy of the strategy.

The average win was positively impacted by Bitcoin’s earlier smaller market cap, as the percentage wins earlier were higher.

Overall the strategy shows potential for further development and may be suitable for walk-forward testing and out of sample analysis to be considered for a demo trading account.

Note in an actual trading setup, you may wish to use this with volatility filters, combined with support resistance zones for a better setup.

As always, this post/indicator/strategy is not financial advice, and please do your due diligence before trading this live.

Original indicator links:

On chart version -

Oscillator version -

Update - 27/06/2022

Unfortunately, It appears that the original script had been taken down due to auto-moderation because of concerns with no slippage / commission. I have since adjusted the backtest, and re-uploaded to include the following to address these concerns, and show that I am genuinely trying to give back to the community and not mislead anyone:

1) Include commission of 0.1% - to match Binance's maker fees prior to moving to a fee-less model.

2) Include slippage of 10 ticks (This is a realistic slippage figure from searching online for most crypto exchanges)

3) Adjust account balance to 10,000 - since most of us are not millionaires.

The rest of the backtesting parameters are comparable to previous results:

Backtesting parameters:

Initial capital: 10000 dollars

Position size: 10% of equity

Long stop: 2% below entry

Short stop: 2% above entry

Repainting: Off

Smoothing: SMA

Period: 10

Slippage: 10 ticks

Commission: 0.1%

This script still remains to shows viability / profitablity on higher term timeframes (with slightly higher drawdown), and I have included the backtest report below to document my findings:

8 Hour:

Number of Trades: 1082

Gross Return: 233.02%

CAGR Return: 14.04 %

Max Drawdown: 7.9 %

Win percentage: 25.6%

Profit Factor (Expectancy): 1.627

Average Loss: 0.46 %

Average Win: 2.18 %

Average Time for Loss: 1.33 day

Average Time for Win: 7.33 days

Once again, please do your own research and due dillegence before trading this live. This post is for education and information purposes only, and should not be taken as financial advice.

BEST Strategy Template w/ Custom SL/TP Size - EducationalHello traders

I'm getting this question at least once per week: "how to define a custom exit quantity for my stop loss and a different one for my take profit"

Instead of answering every day the same question in my DMs, I've decided to publish an educational strategy template script using this

Features

- Select to use or not the SL and/or TP

- Define how many pips/USD the SL/TP should be set at from the entry

- Define what quantity percentage you want to close at SL and/or at TP (lines 301 to 320 in the code)

- Classical custom trailing stop where the SL is moved to breakeven once the TP is hit

- Get real-time backtesting stats based on the options you've selected

Update

You might not know it yet but from last week (or maybe the week before), the qty/qty_percent from the strategy.exit function refers now to the initial position size (and not the remaining position size like before)

For example:

strategy.exit("EX1", qty_percent = 50, stop = constant)

strategy.exit("EX2", qty_percent = 20, stop = constant)

What happened before

After "EX1" reaches SL levels, "EX2" exits 20% from the % of the remaining position size.

If the initial position size = 100 contracts

EX1 exits 50 contracts

EX2 exits 20% of 50 contracts = 10 contracts

What's happening now

After "EX1" reaches SL levels, "EX2" exits 20% from the % of the original position size.

If the initial position size = 100 contracts

EX1 exits 50 contracts

EX2 exits 20 (20% of 100 contracts) contracts

I think this is an improvement and I really enjoy this new behavior.

See you in a few days with another post :)

ALL THE BEST

Dave

Gap Reversion StrategyToday I am releasing to the community an original short-term, high-probability gap trading strategy, backed by a 20 year backtest. This strategy capitalizes on the mean reverting behavior of equity ETFs, which is largely driven by fear in the market. The strategy buys into that fear at a level that has historically mean reverted within ~5 days. Larry Connors has published useful research and variations of strategies based on this behavior that I would recommend any quantitative trader read.

What it does:

This strategy, for 1 day charts on equity ETFs, looks for an overnight gap down when the RSI is also in/near an oversold position. Then, it places a limit order further below the opening of the gapped-down day. It then exits the position based on a higher RSI level. The limit buy order is cancelled if the price doesn't reach your limit price that day. So, the larger you make the gap and limit %, the less signals you will have.

Features:

Inputs to allow the adjustment of the limit order %, the gap %, and the RSI entry/exit levels.

An option to have the limit order be based on a % of ATR instead of a % of asset price.

An optional filter that can turn-off trades when the VIX is unusually high.

A built in stop.

Built in alerts.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

BB + RSI double strategy developeI'm Korean, and it may not be enough to explain this script in English. I feel sorry for the users of TradingView for this lack of English skills. If you are Korean, please return it to the translator using Papago. It will be a useful manual for you.

This script referenced Chartart's Double Strategy. But there are some changes in his script.

0. Basically, when you break through the top or bottom of the 100th period balliser band and come back into the band, you track the overbuying and overselling of the RSI to determine your position entry. The order is triggered only when both conditions are satisfied at the same time. However, only one condition applies to clearing the position. This is because it is most effective in reducing risk and increasing assets in terms of profit and loss.

1. This script is optimized for 15 minutes of bitcoin futures chart and API via webbook alert. By default, 10x leverage usage and 10 pyramids are applied.

2. Setting a chart period other than 15 minutes will not guarantee sufficient effectiveness. It can also be applied to Ethereum , but it is not recommended to apply to other symbols.

3. I added Enable Date Filter because Chartart's script could not apply the strategy to the user's desired period. This feature allows you to set a period of time when you do not want to use the strategy. You can also uncheck it if you don't want to fully use this feature. Please remember that it is an exclusion period, not a usage period. With this feature, we can see the effectiveness of the strategy from a point in time, not from the entire period. You can also clearly differentiate the effectiveness of the strategy from the point you use it.

4. You can also stop using strategies at certain times of the day when you don't want to apply them. This works similarly to the Enalbe Date Filter described above. This allows you to sleep comfortably even if you don't fully trust this strategy.

5. The period, overbuying, and overselling figures of RSI can be set individually. For example, when you take a long position, you can set the RSI to a period of 7, and at the same time, the RSI entering the short position can be set to a period of 14. You can also set the base figures for overbuying and overselling to levels that you think are reasonable. This figure works in conjunction with the Bollinger Band and affects position entry when it is crossed or returned.

6. Based on API futures trading, basic Sleepy and commission are applied. This is geared towards market price transactions. This makes your revenue look more reasonable.

Thank you very much, Chartart. You are a genius.

-

저는 한국인이고, 영어로 이 스크립트를 설명하는 것이 어렵기 때문에 설명이 부족할 수 있습니다. 이런 영어 능력 부족에 대해서 TradingView 사용자들에게 미안하게 생각합니다. 만약 당신이 한국인이라면 파파고를 사용하여 번역기에 돌려주십시오. 당신에게 유익한 설명서가 될 것입니다.

이 스크립트는 Chart art의 Double Strategy를 참조했습니다. 그러나 그의 스크립트에서 달라진 점이 몇 가지 있습니다.

0. 기본적으로 100기간의 볼린져밴드의 상단 또는 하단을 돌파한 뒤 다시 밴드 안으로 들어올 때 RSI의 과매수, 과매도를 추적하여 포지션 진입을 결정합니다. 두 가지 조건이 동시에 만족되어야만 주문이 트리거 됩니다. 그러나 포지션을 청산하는 것에는 볼린져밴드 하나의 조건만 적용합니다. 여러가지 테스트를 거친 결과 이것이 손익 면에서 가장 효과적으로 리스크를 줄이고 자산을 늘리는 것에 효율적이기 때문입니다.

1. 이 스크립트는 15분의 비트코인 선물 차트와 webhook alert을 통한 API에 최적화되어 있습니다. 기본적으로 10배의 레버리지 사용과 10개의 피라미딩이 적용되어 있습니다.

2. 15분 외에 다른 차트 기간을 설정한다면 충분한 효과를 보장할 수 없습니다. 또한 이더리움에도 적용할 수 있지만, 그 외에 다른 심볼에는 적용하지 않는 것을 권장합니다.

3. Chart art의 스크립트는 전략을 사용자가 원하는 기간에 적용할 수 없었기 때문에, 저는 Enable Date Filter를 추가하였습니다. 이 기능을 통해 전략 사용을 원하지 않는 기간을 설정할 수 있습니다. 또한 이 기능을 완전히 사용하고싶지 않다면 체크를 해제할 수 있습니다. 사용 기간이 아닌 제외 기간인 점을 상기하시길 바랍니다. 이 기능을 통해 우리는 전체 기간이 아닌 가까운 특정 시점부터의 전략 적용 효과를 확인할 수 있습니다. 또한 사용자가 전략을 사용한 시점부터의 효과를 명백히 구분할 수 있습니다.

4. 또한 사용자가 적용을 원하지 않는 하루 중의 특정 시간대에 전략 사용을 멈출 수도 있습니다. 이는 위에 설명한 Enalbe Date Filter와 유사하게 작동합니다. 이를 통해 당신이 온전히 이 전략을 신뢰하지 못하여도 당신은 마음 편하게 잠에 들 수 있습니다.

5. RSI의 기간 및 과매수, 과매도 수치를 개별적으로 설정할 수 있습니다. 예를 들어 당신이 롱 포지션을 취할 때에는 RSI를 7의 기간으로 설정할 수 있고, 동시에 숏 포지션을 진입하는 RSI는 14의 기간으로 설정될 수 있습니다. 또한 과매수 및 과매도의 기준 수치를 당신이 합리적이라고 생각하는 수준으로 설정할 수 있습니다. 이 수치는 볼린져밴드와 함께 작동하여 그것을 넘어서거나 다시 되돌아올 때 포지션 진입에 영향을 미칩니다.

6. API 선물거래를 기준으로 하여 기본적인 슬리피지와 커미션이 적용되어있습니다. 이는 시장가 거래에 맞춰져 있습니다. 이는 당신의 수익을 좀 더 합리적인 수치로 보일 수 있게 합니다.

Chartart에게 특별히 감사합니다. 당신은 천재입니다.

EMA bands + leledc + bollinger bands trend following strategy v2The basics:

In its simplest form, this strategy is a positional trend following strategy which enters long when price breaks out above "middle" EMA bands and closes or flips short when price breaks down below "middle" EMA bands. The top and bottom of the middle EMA bands are calculated from the EMA of candle highs and lows, respectively.

The idea is that entering trades on breakouts of the high EMAs and low EMAs rather than the typical EMA based on candle closes gives a bit more confirmation of trend strength and minimizes getting chopped up. To further reduce getting chopped up, the strategy defaults to close on crossing the opposite EMA band (ie. long on break above high EMA middle band and close below low EMA middle band).

This strategy works on all markets on all timeframes, but as a trend following strategy it works best on markets prone to trending such as crypto and tech stocks. On lower timeframes, longer EMAs tend to work best (I've found good results on EMA lengths even has high up to 1000), while 4H charts and above tend to work better with EMA lengths 21 and below.

As an added filter to confirm the trend, a second EMA can be used. Inputting a slower EMA filter can ensure trades are entered in accordance with longer term trends, inputting a faster EMA filter can act as confirmation of breakout strength.

Bar coloring can be enabled to quickly visually identify a trend's direction for confluence with other indicators or strategies.

The goods:

Waiting for the trend to flip before closing a trade (especially when a longer base EMA is used) often leaves money on the table. This script combines a number of ways to identify when a trend is exhausted for backtesting the best early exits.

"Delayed bars inside middle bands" - When a number of candle's in a row open and close between the middle EMA bands, it could be a sign the trend is weak, or that the breakout was not the start of a new trend. Selecting this will close out positions after a number of bars has passed

"Leledc bars" - Originally introduced by glaz, this is a price action indicator that highlights a candle after a number of bars in a row close the same direction and result in greatest high/low over a period. It often triggers when a strong trend has paused before further continuation, or it marks the end of a trend. To mitigate closing on false Leledc signals, this strategy has two options: 1. Introducing requirement for increased volume on the Leledc bars can help filter out Leledc signals that happen mid trend. 2. Closing after a number of Leledc bars appear after position opens. These two options work great in isolation but don't perform well together in my testing.

"Bollinger Bands exhaustion bars" - These bars are highlighted when price closes back inside the Bollinger Bands and RSI is within specified overbought/sold zones. The idea is that a trend is overextended when price trades beyond the Bollinger Bands. When price closes back inside the bands it's likely due for mean reversion back to the base EMA in which this strategy will ideally re-enter a position. Since the added RSI requirements often make this indicator too strict to trigger a large enough sample size to backtest, I've found it best to use "non-standard" settings for both the bands and the RSI as seen in the default settings.

"Buy/Sell zones" - Similar to the idea behind using Bollinger Bands exhaustion bars as a closing signal. Instead of calculating off of standard deviations, the Buy/Sell zones are calculated off multiples of the middle EMA bands. When trading beyond these zones and subsequently failing back inside, price may be due for mean reversion back to the base EMA. No RSI filter is used for Buy/Sell zones.

If any early close conditions are selected, it's often worth enabling trade re-entry on "middle EMA band bounce". Instead of waiting for a candle to close back inside the middle EMA bands, this feature will re-enter position on only a wick back into the middle bands as will sometimes happen when the trend is strong.

Any and all of the early close conditions can be combined. Experimenting with these, I've found can result in less net profit but higher win-rates and sharpe ratios as less time is spent in trades.

The deadly:

The trend is your friend. But wouldn't it be nice to catch the trends early? In ranging markets (or when using slower base EMAs in this strategy), waiting for confirmation of a breakout of the EMA bands at best will cause you to miss half the move, at worst will result in getting consistently chopped up. Enabling "counter-trend" trades on this strategy will allow the strategy to enter positions on the opposite side of the EMA bands on either a Leledc bar or Bollinger Bands exhaustion bar. There is a filter requiring either a high/low (for Leledc) or open (for BB bars) outside the selected inner or outer Buy/Sell zone. There are also a number of different close conditions for the counter-trend trades to experiment with and backtest.

There are two ways I've found best to use counter-trend trades

1. Mean reverting scalp trades when a trend is clearly overextended. Selecting from the first 5 counter-trend closing conditions on the dropdown list will usually close the trades out quickly, with less profit but less risk.

2. Trying to catch trends early. Selecting any of the close conditions below the first 5 can cause the strategy to behave as if it's entering into a new trend (from the wrong side).

This feature can be deadly effective in profiting from every move price makes, or deadly to the strategy's PnL if not set correctly. Since counter-trend trades open opposite the middle bands, a stop-loss is recommended to reduce risk. If stop-losses for counter-trend trades are disabled, the strategy will hold a position open often until liquidation in a trending market if th trade is offsides. Note that using a slower base EMA makes counter-trend stop-losses even more necessary as it can reduce the effectiveness of the Buy/Sell zone filter for opening the trades as price can spend a long time trending outside the zones. If faster EMAs (34 and below) are used with "Inner" Buy/Zone filter selected, the first few closing conditions will often trigger almost immediately closing the trade at a loss.

The niche:

I've added a feature to default into longs or shorts. Enabling these with other features (aside from the basic long/short on EMA middle band breakout) tends to break the strategy one way or another. Enabling default long works to simulate trying to acquire more of the asset rather than the base currency. Enabling default short can have positive results for those high FDV, high inflation coins that go down-only for months at a time. Otherwise, I use default short as a hedge for coins that I hold and stake spot. I gain the utility and APR of staking while reducing the risk of holding the underlying asset by maintaining a net neutral position *most* of the time.

Disclaimer:

This script is intended for experimenting and backtesting different strategies around EMA bands. Use this script for your live trading at your own risk. I am a rookie coder, as such there may be errors in the code that cause the strategy to behave not as intended. As far as I can tell it doesn't repaint, but I cannot guarantee that it does not. That being said if there's any question, improvements, or errors you've found, drop a comment below!

Estrategia Larry Connors [JoseMetal]============

ENGLISH

============

- Description:

This strategy is based on the original Larry Connors strategy, using 2 SMAs and RSI.

The strategy has been optimized for better total profit and works better on 4H (tested on BTCUSDT).

LONG:

Price must be ABOVE the slow SMA.

When a candle closes in RSI oversold area, the next candle closes out of the oversold area and the closing price is BELOW the fast SMA = open LONG.

LONG is closed when a candle closes ABOVE the fast SMA.

SHORT:

Price must be BELOW the slow SMA.

When a candle closes in RSI overbought area, the next candle closes out of the overbought area and the closing price is ABOVE the fast SMA = open SHORT.

SHORT is closed when a candle closes BELOW the fast SMA.

*Larry Connor's strategy does NOT use a fixed Stop Loss or Take Profit, as he said, that reduces performance significantly.

- Visual:

Both SMAs (fast and slow) are shown in the chart.

By default, the fast SMA is aqua color, the slow changes between green and red depending on the "trend" (price over slow SMA = bullish, below = bearish).

RSI can't be shown because TradingView doesn't allow to show both overlay and panel indicators, so candles get a RED color when RSI is in OVERBOUGHT area and GREEN when they're on OVERSOLD area to help with that.

Background is colored when conditions are met and a position is going to be open, green for LONGs red for SHORTs.

- Usage and recommendations:

As this is a coded strategy, you don't even have to check for indicators, just open and close trades as the strategy shows.

The original strategy uses a 5 period SMA instead of the 10, and 10/90 for oversold/overbought levels, this has been optimized after the testings and results but feel free to change settings and test by yourself.

Also, the original strategy was developed for daily, but seems to work better en 4H.

- Customization:

As usual I like to make as many aspects of my indicators/strategies customizable, indicators, colors etc., feel free to ask if you feel that something that should be configurable is missing or if you have any ideas to optimize the strategy.

============

ESPAÑOL

============

- Descripción:

Esta estrategia está basada en la estrategia original de Larry Connors, utilizando 2 SMAs y RSI.

La estrategia ha sido optimizada para un mejor beneficio total y funciona mejor en 4H (probado en BTCUSDT).

LONG:

El precio debe estar por encima de la SMA lenta.

Cuando una vela cierra en la zona de sobreventa del RSI, la siguiente vela cierra fuera de la zona de sobreventa y el precio de cierre está POR DEBAJO de la SMA rápida = abre LONG.

Se cierra cuando una vela cierra POR ENCIMA de la SMA rápida.

SHORT:

El precio debe estar POR DEBAJO de la SMA lenta.

Cuando una vela cierra en la zona de sobrecompra del RSI, la siguiente vela cierra fuera de la zona de sobrecompra y el precio de cierre está POR ENCIMA de la SMA rápida = abre SHORT.

Se cierra cuando una vela cierra POR DEBAJO de la SMA rápida.

*La estrategia de Larry Connor NO utiliza un Stop Loss o Take Profit fijo, como él dijo, eso reduce el rendimiento significativamente.

- Visual:

Ambas SMAs (rápida y lenta) se muestran en el gráfico.

Por defecto, la SMA rápida es de color aqua, la lenta cambia entre verde y rojo dependiendo de la "tendencia" (precio por encima de la SMA lenta = alcista, por debajo = bajista).

El RSI no puede mostrarse porque TradingView no permite mostrar tanto los indicadores superpuestos como los del panel, así que las velas obtienen un color ROJO cuando el RSI está en el área de SOBRECOMPRA y VERDE cuando están en el área de VENTA para ayudar a ello.

El fondo se colorea cuando se cumplen las condiciones y se va a abrir una posición, verde para LONGs rojo para SHORTs.

- Uso y recomendaciones:

Como se trata de una estrategia ya programada, ni siquiera hay que comprobar los indicadores, sólo hay que abrir y cerrar las operaciones tal y como muestra la estrategia en el gráfico.

La estrategia original utiliza una SMA de 5 periodos en lugar de 10, y 10/90 para los niveles de sobreventa/sobrecompra, esto ha sido optimizado después de las pruebas y los resultados, pero sé libre de cambiar la configuración y probarla por sí mismo.

Además, la estrategia original fue desarrollada para diario, pero parece funcionar mejor en 4H.

- Personalización:

Como siempre me gusta hacer personalizables todos los aspectos de mis indicadores/estrategias, indicadores, colores, etc., preguntar si notas que falta algo que debería ser configurable o si tienes alguna idea para optimizar la estrategia.